4 AIM Chips that may 'ketch-up'

#NXQ, #TON, #ZYT, #ETP

Disclaimer: I may or may not hold positions in any of the securities or companies discussed in this report. All opinions are my own and are provided for informational purposes only, not as investment advice. Readers should conduct their own research and analysis before making any investment decisions.

The purpose of this newsletter format is to bring you along on my journey of uncovering interesting investment opportunities, companies that may ketch-up (catch up) to a more fair value. Since I am closely following the companies featured in my newsletter, I’ll occasionally update you on their recent developments or performance.

I may also cover one ore more positions of the newsletter in a dedicated write-up if I think it’s time to do so and it makes sense.

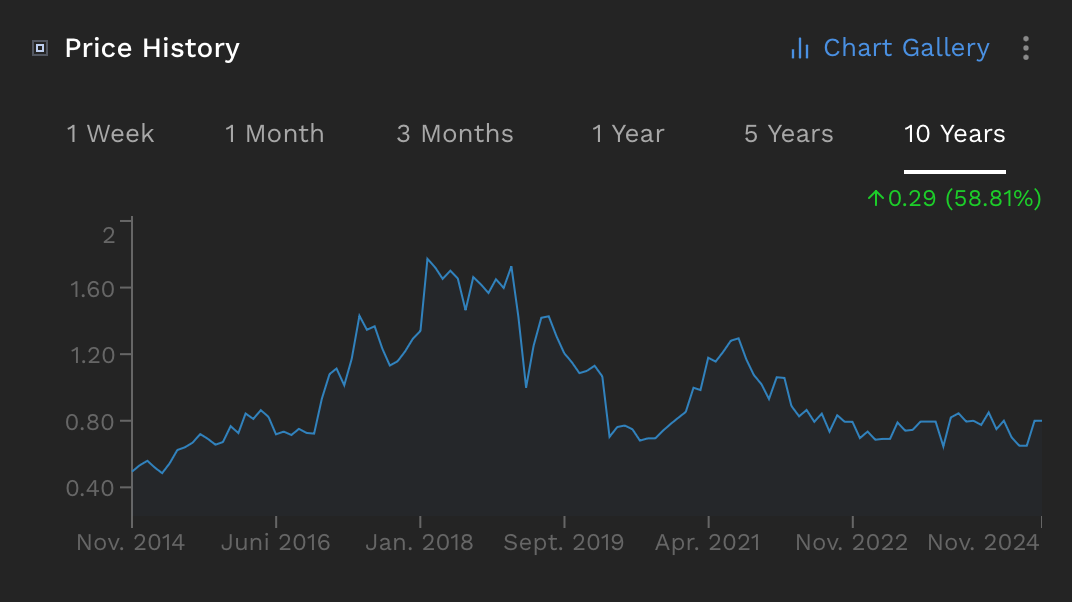

#1 Nexteq (NXQ.L) - What’s next?

Nexteq, formerly Quixant, provides computing hardware under the brand Quixant as well as displays and broadcasting equipment under the brand name Densitron (acquired in 2015) to a variety of industries with focus on the casino/gaming market.

What happened

Recently, the company’s CEO, CFO and chair resigned all of a sudden - during a time when the company suffered from declining revenues. While the market can only speculate about the ‘Why’, the market continues to be challenging with the latest trading update warning that customers continue to destock throughout FY25 resulting in near-term underperformance vs. market expectations.

Why it may ketch-up

The company trades at a market-cap of 44m with 30m cash on the bank (actually even more but I took the expected cash at year end due to buy-backs) + tangible assets and inventories. So you pay for their tangible assets and get the operating business for free - a not so bad deal? The company has no debt, has been profitable throughout its history and is about to present a growth plan in Q1 ‘25. Given the cash pile and ongoing profitability I wouldn’t be surprised to see a new acquisition in adjacent markets in the next 1-2 years.

In April ‘24 the company extended a share-buyback up to 10% of their issued share capital (3% of which is still to be bought back). The new CEO Duncan Faithfull has been the former commercial director of the gaming segment and seems to be very capable. He is currently undertaking a detailed business review for organic growth opportunities. Matt Staight, former financial controller, was recently appointed CFO.

Potential Upside

You rarely see a quality business trading at a discount to NAV. Should the current issues prove to be of temporary nature (not extending beyond FY25) 100% upside or c. 90m market-cap is the absolute minimum a growth business with c. 90m revenues, 10% PBT margins and a strong balance sheet would deserve. Investor presentations (take it with a grain of salt) indicate that the company’s products are still in high demand and capable to further penetrate markets. The company also points out that the model of outsourcing key parts for OEMs can be adapted to other verticals as well.

#2 Titon (TON.L) - A breath of fresh air?

Titon is a manufacturer of door & window hardware and ventilation systems and has been alive for 50 years.

What happened

Titon has a history of profitability (albeit low with 5% operating margins) but has underperformed in recent years. In addition to that the company has experienced a period of high executive turnover, with three CEOs taking the helm in quick succession. Insiders have also sold shares even after Harwood acquired a stake which confused investors.

Why it may ketch-up

The company’s new CEO Tom Carpenter (joined in April ‘24) has started an internal review with the result being a refreshed business strategy focusing on sales growth and renewed focus on the window & door segment. Further, the company divested its interest from an underperforming Joint Venture in Korea.

The company evaluates also its go-to-market strategy with a potential focus on the social housing market. Competitors are highly profitable with operating margins north of 10%.

Having a market-cap of 8.7m and a pro-forma EV of c. 5m after divesture, Titon trades at a discount to its conservatively adj. tangible NAV of ca. 10m providing downside protection. Harwood Capital which is known for driving shareholder value through activism holds 28% of outstanding shares. The last RNS informed that the Chair Jamie Brooke and CEO bought shares and now hold 0.9% and 0.6% of the share capital respectively. I wouldn’t put too much emphasis on that, as Tom announced in the last earnings call “he will buy if he is be able to do so” (black-out period).

Potential Upside

If the company can demonstrate its ability to grow and achieve the scale needed to improve operating profit, a valuation of 2x book value — aligned with 1x sales for a 10% operating margin — appears realistic, offering a potential upside of 150%. While this won’t happen overnight it is definitely achievable in the next 2-4 years.

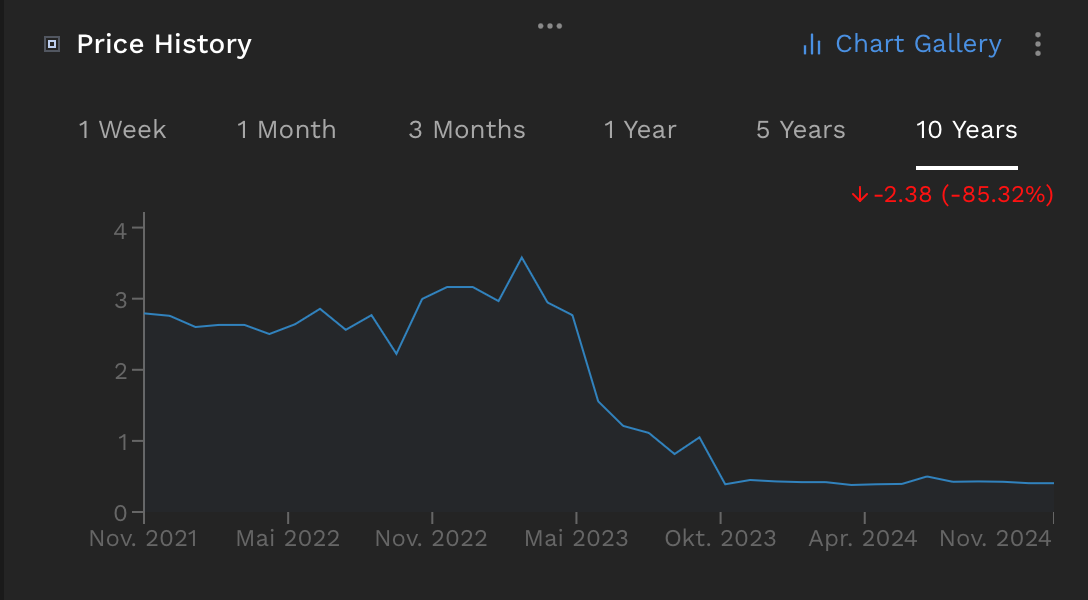

#3 Zytronic (ZYT.L) - Who votes for liqui-tronic?

Zytronic develops and manufactures the electronic part of touchscreens which they supply to OEMs.

What happened

The company had suffered from a serious revenue and profitability decline since FY17 which forced the company to rethink its business strategy. The outcome of an internal review resulted in 5 options being presented to shareholders: Transformation, Liquidation, Sale of the company, Delisting or Cash-Shell.

Recently the company posted a trading update for FY24 including the announcement of a strategic review under the Takeover-Code with options outlined earlier to be discussed in alignment with shareholders.

Why it may ketch-up

Looking at the flow of 8.3 filings it seems feasible (at least in theory) to achieve a 75% majority for a special resolution voting for a liquidation. The reason is that most shareholders holding >1% are asset-managers focused on shareholder value including Swedish value investor Peter Gyllenhammar and there are no notable insiders who could oppose such a voting except a former NED holding 5% and the CEO and CFO holding 1-2%. The formal strategy review was announced after PG built a position - coincidence? Further, PG and Henry Spain Investment Services have been increasing their stake slightly during the review period.

Potential Upside

Zytronic trades at c. 49 pence per share, while its NAV/share is estimated to be 127 pence. This means that a liquidation would create almost immediate shareholder value assuming the 127 pence liquidation value can be achieved. In contrast, a transformation would cost an estimated 2.5m to 3.5m and take another 4-5 years with the outcome being uncertain and the book value being burned down further - leaving shareholders with potentially nothing. This is a bet on a near-term sale or liquidation and that a 75% voting majority can be reached. In the end it’s a bet that significant shareholders hold a similar opinion.

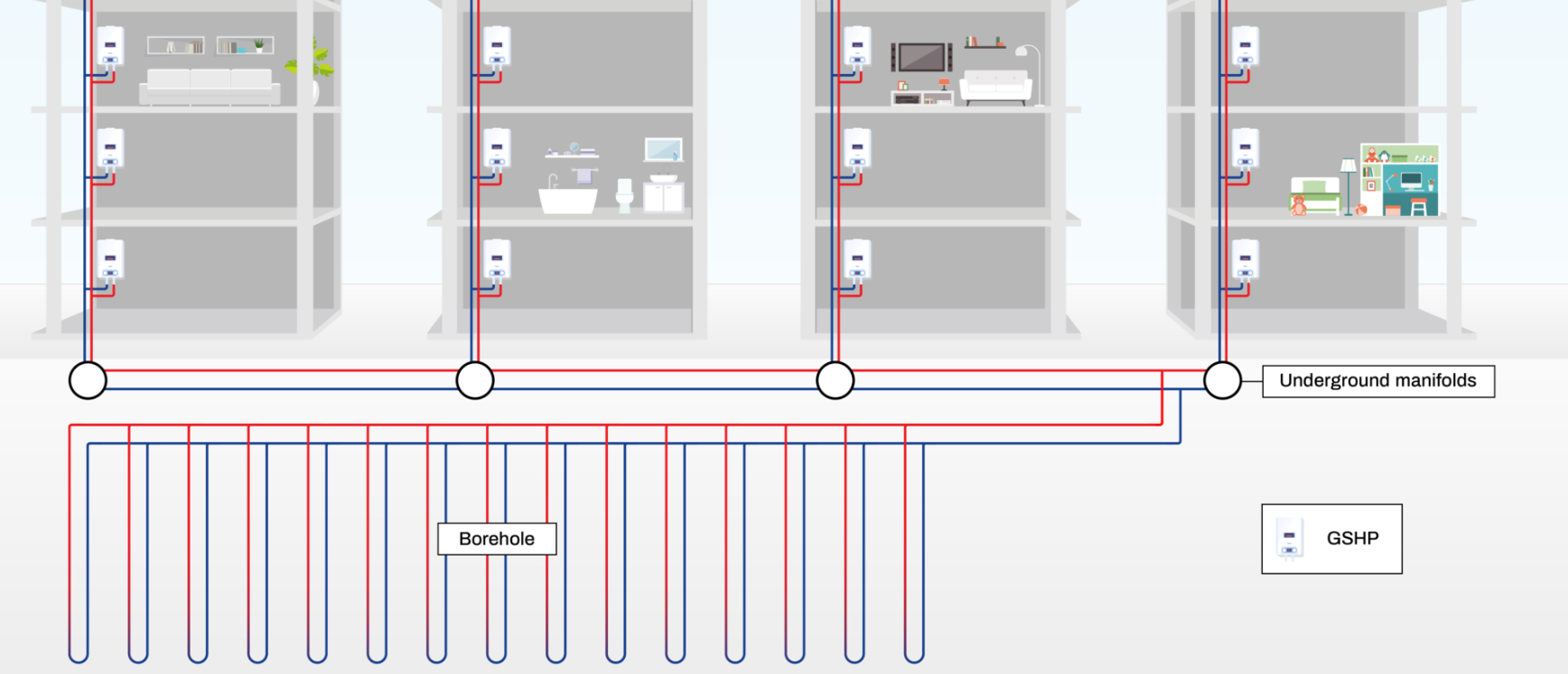

#4 Eneraqua (ETP.L) - Zero Profit or Profit from Net Zero?

Eneraqua provides installation services for various sorts of heat pumps to the domestic (and increasingly) non-domestic commercial sector and provides also water saving solutions by deploying their IP-based flowcontrol device.

What happened

Eneraqua went public in 2021 and posted solid results in the subsequent 2 years. However, in 2023 things worsened and the company posted a profit warning and later horrendous results for FY24: Gross margins halved, admin expenses increased, revenue growth was negative and a loss was posted. What a mess... And FY25 did not progress much better. H1 printed a loss, but H2 is expected to be profitable again, albeit with a 60% weighting making it more prone to execution risk.

Why it may ketch-up

In my opinion there is a clear mismatch between Eneraqua’s market-cap of 13m (down from almost 90m when it IPOed) with almost no debt against its current order book of 118m (40% of which Is expected to be delivered in H2 ‘25) and its pipeline of opportunities worth 300m (40% anticipated win-rate). There is also strong insider ownership of 30%.

While the recent underperformance is puzzling and so are the CEO’s excuses (“project-mix”, non-domestic projects have lower margins, delayed orders due to budget, unclear policy around decarbonisation funds, elections in UK) it is encouraging that installation businesses typically boost gross margins of 40%+ (while Eneraqua’s gross margins are down to 20%). So keeping the big picture in mind operating an installation business has proven to be profitable for many companies. So I think neither the losses in the last one and a half years nor the minuscule margins are the new normal for the business.

Eneraqua has also a water segment which is, probably because of its still negligible top-line impact, entirely neglected but has the medium- to long-term potential to contribute significantly to the bottom-line as margins in this segment are materially higher. Observing the news flow for Eneraqua it looks like they put an increasing emphasis on this segment and convert also an increasing number of customers.

There are also huge tailwinds through the self-imposed Net zero agenda by EU and UK (each has their own target) requiring an increasing number of heat pumps to be installed to meet the goals.

Potential Upside

With a current revenue run-rate of 80m+ for the financial years ‘25 and beyond it is obvious how cheap Eneraqua is in case they get back to operating margins between 5 and 10% when operating leverage kicks in the right direction. For instance, based on their FY ‘25 forecast the company trades at 2.2 x EV/EBITDA and based on FY ‘26 they trade at 1.6 x EV/EBITDA while competitors trade at around 5x EBITDA. Keep in mind that the financial year ends in January for Eneraqua. So FY25 is already in January ‘25 and FY26 is already in a little more than one year time.

Assuming 0.5 x sales valuation for 5% operating margin and 1 x sales for 10% operating margin (blue sky scenario), the company would be worth between 40m and 80m.

While Eneraqua (due to its asset-light business model) doesn’t give a lot of downside protection if operations or market conditions continue to deteriorate, it provides a significant upside which makes up for that.

On what company would you like a full write-up?